Introduction

At the moment global economy is facing massive inflation. This has forced US Federal Reserve to raise interest rate to stem in inflation inside USA. This in turn has lured private lenders away from Emerging Economies (EMEs), Least Developing Countries (LDCs) and even Developed Economies (DEs) like EU and Japan and China to USA. The lenders will go where they will get maximum interest income. As a result many EMEs and LDCs are facing lack of foreign credit in global market and hence they are running short of foreign exchange. Often their foreign exchange reserves are so low that they cannot cover more than 3 months imports. Continuous flowing out of foreign exchange mainly US Dollars result in devaluation of domestic currencies against US Dollar. This inflates the bills of necessary imports. High oil-food-fertilizer prices have increased their import bills further aggravating the shortage of foreign exchange crisis. Now this article will discuss how EMEs and LDCs can mitigate this problem by using prudent currency exchange between themselves and by bargaining with private lenders of global market.

Problem Is Not Temporary

This problem of high inflation and costly credit in global market is not a temporary phenomenon. The problem is much more systemic and there is no short term remedy. We must remember that in 1970s global economy started to face stagflation i.e. low economic growth with high inflation. Many economists pointed out that oil price hike by OPEC under leadership of Saudi Arabia from 1973 to 1979 was the main reason for stagflation. From 1980s inflation started going down and global economy started to grow. The main cause of end of stagflation was actually introduction of China in global market in 1980s. China with its massive scale of productive cheap workers entered the global market and started to produce at cheaper price. Thus inflation began to cool down and supply rose significantly in the global market. Low inflation helped all central banks including US Federal Reserve to keep interest rate low. Thus low inflation resulted in rise of cheap credit in the global market. This cheap credit financed many economic activities including unproductive ones in EMEs, LDCs and DEs. This cheap credit helped many EMEs and LDCs to consume beyond their ability to produce and also helped DEs to invest in profitable yet unproductive asset trading.

But after four decades of record growth China's workers are no longer cheap. Wage rate has grown 5 times in four decades. China is now a Developed Economy and its total economy has expanded its growth rate has moderated compared to last decade. Naturally China's ability to keep inflation low in global market has been reduced significantly by 2020s. Thus source of cheap credit is drying up as well. Geopolitical clash between declining USA and rising China (two largest economies in the world), has distorted global chain adding to inefficiency and hence global inflation. Russian military operation in Ukraine and USA's decision to help Ukraine has further raised global inflation as Russia despite being 2% of global GDP is an important supplier of daily necessities like oil, gas, fertilizer and grain. Pelosi's Taiwan visit clearly shows geopolitical clashes between USA and China-Russia will only rise. So high inflation and costly credit are now permanent reality with which world has to live with.

Use Of Multi Currencies Is The Way To Go

Since inflation and high interest are here to stay, EMEs and LDCs will keep facing shortage of US Dollar as private global creditors will keep pulling out US Dollars from EMEs and move to USA and other DEs. So EMEs and LDCs have to chalk out a long term strategy to counter this. They have to tackle this in three ways simultaneously. One is through current account, second is through capital account and third is by raising productivity of the economy.

Current Account Solution

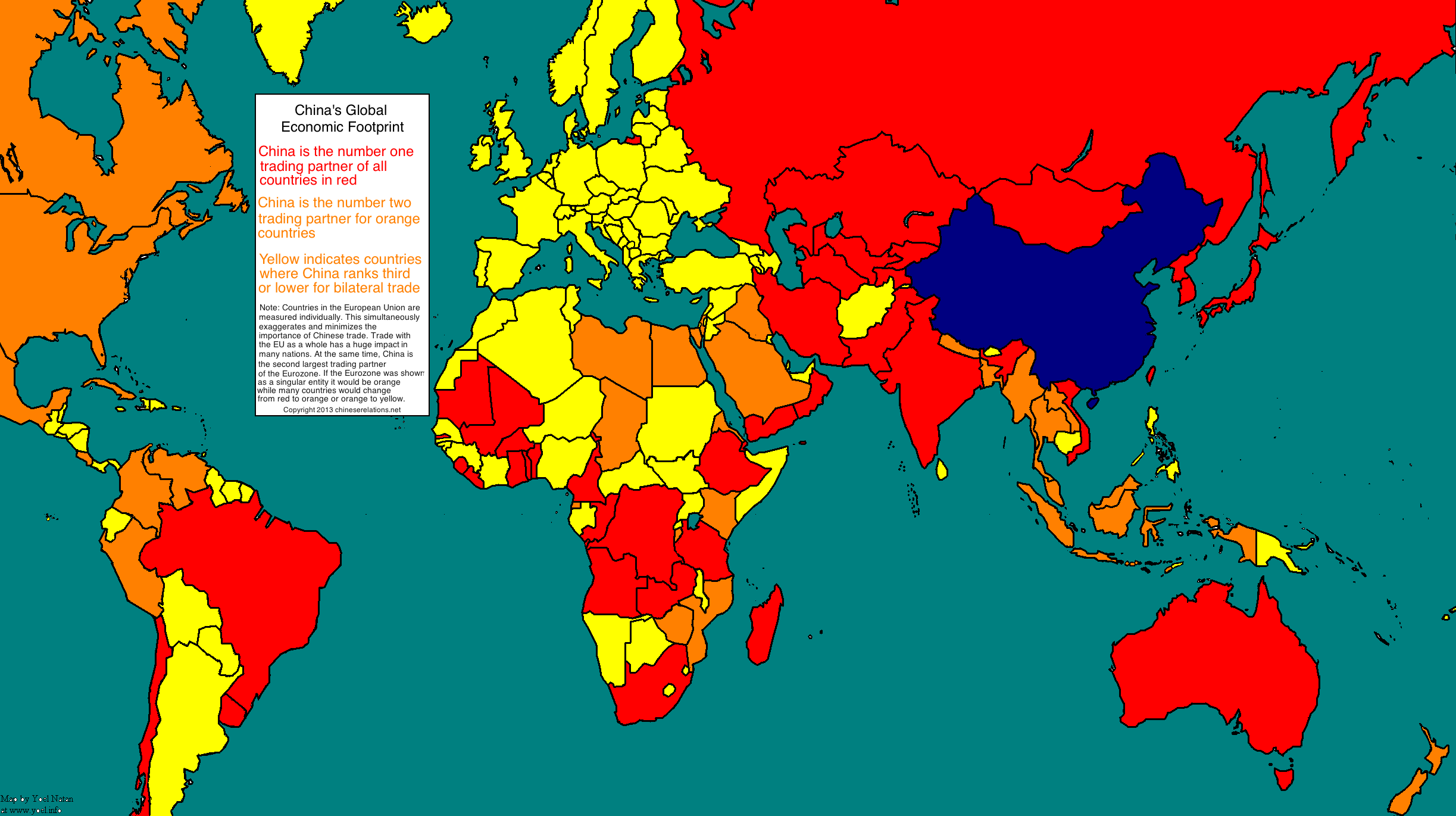

EMEs and LDCs must deal bilateral trade with currencies other than US Dollar. China is largest bilateral trading partner or second largest bilateral trading partner for almost all EMEs and LDCs. So they must trade with China more in Chinese currency Yuan. Many EMEs and LDCs may also start trading among themselves with Yuan too. Similarly they can use currency of other important partner countries who usually have trade surplus with the former ones. Selective use of other big economies like EU's Euro and Japan's Yuan can be used too. In this way, EMEs and LDCs can maintain their minimum import level without any use of US Dollar. It must be remembered that USA is most important bilateral trading partner of most countries. So remittances inflow must be encouraged in US Dollar. Moreover, big economies who have no shortage of US Dollar must be asked to pay partly in US Dollar. For example, Sri Lanka must trade with China partly in Yuan and partly in US Dollar. Sri Lanka must trade with other EMEs in mostly Yuan and also partly in Rubles, Yen, Euro and partner country's currency. Gold and other valuable metals can be used too. This is best way to continue imports for most of EMEs and LDCs. Russia is already working on this model where it is dealing with Yuan and many of partners' currencies instead of US Dollar and Euro. Turkiye too is seeming to follow Russia's path. Brazil and India also are partly following the same rule.

Capital Account Solution

The main strength of US Dollar is not its role in product market but in asset market. US asset market is considered most lucrative by private global lenders. So higher inflation and hence higher interest rate by US Federal Reserve attracts private global lenders to USA in a great way. These private lenders have their head offices mostly in New York and London. They are most important instrument of foreign exchange flow in the global economy. EMEs and LDCs have to force these private global lenders to accept non US Dollars as payment. IMF and World Bank must be asked for accepting interest in multiple currencies. IMF itself has raised weight of Yuan in its SDR basket significantly. EMEs and LDCs must make private lenders accept multiple currencies in weight given by IMF's SDR. These private lenders can be lured to accept non US Dollars if EMEs and LDCs are ready to raise their interest rate in a big way. But this will hamper their economic development as high interest rate will imply lower growth. So most EMEs and LDCs will try to avoid this path.

Productivity Solution

The countries of EMEs and LDCs must deal with private creditors in a united way to make impact. A recession or low growth in USA will surely force these lenders to come to terms with EMEs and LDCs. The higher the growth EMEs and LDCs can achieve compared to USA, the more private creditors will lured towards the former group of countries. Since higher interest rate will ensure lower growth in USA, the rest of the world will surely have higher bargaining power with private lenders in future as growth differential will work in their favor. So EMEs and LDCs must be ready to raise their economies' productivity such that at same interest rate, their growth rate must rise significantly. Keeping interest rate same these countries must invest more by raising propensity to invest and from same amount of investment they must produce more output by raising workers' efficiency and productivity.

Conclusion

If significant portion of imports are covered by non US Dollar transactions and using higher growth EMEs and LDCs can force private global lenders to accept non US Dollar payments then these countries can save themselves from foreign exchange shortage crisis in the coming years. The more attractive Chinese asset market becomes, the more likely global lenders will start accepting Yuan which will mean more advantage to EMEs and LDCs. So the two most important policies are cooperation among non Western countries and unleashing productive potential in each of these countries.

Author: Saikat Bhattacharya